After implementing a central platform for B2G e-invoicing, France initially planned to introduce the Y-Scheme for its B2B mandate, incorporating both a central platform and certified providers.

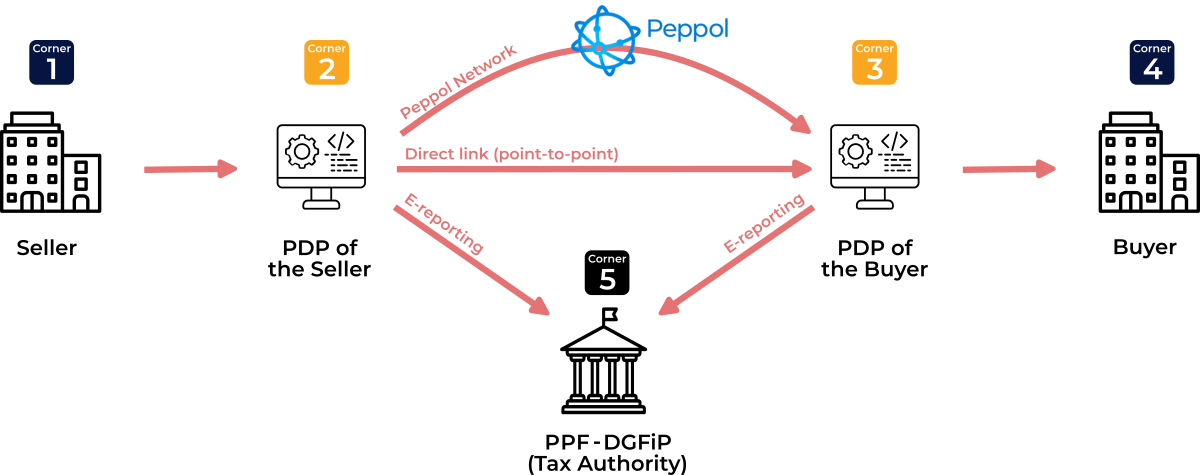

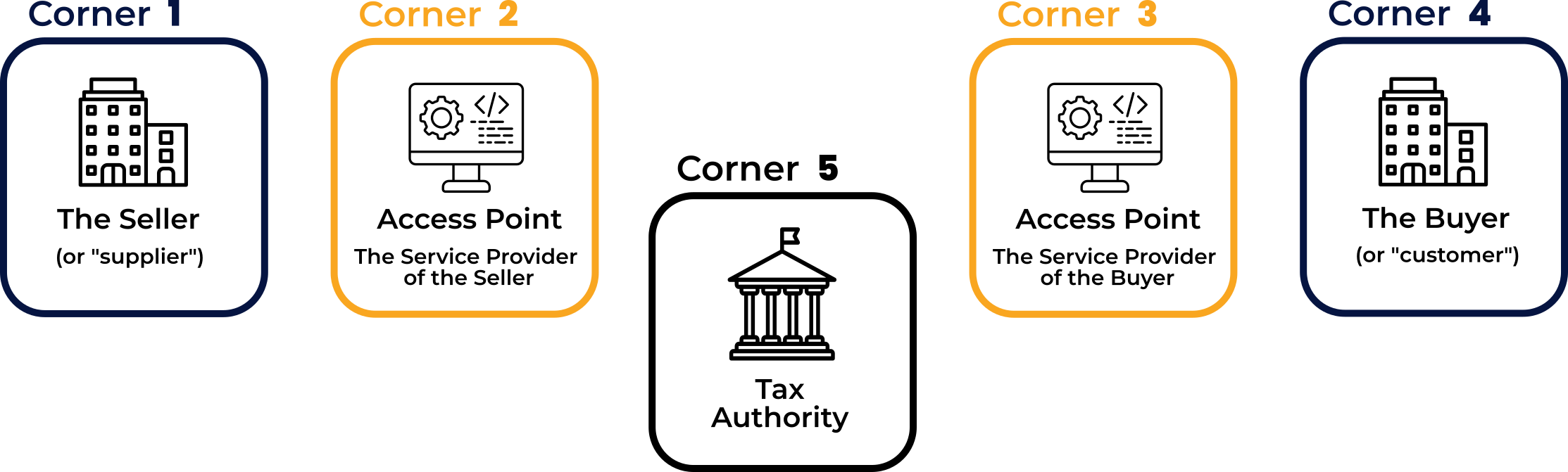

However, due to time and budget constraints, the French government has significantly scaled back the project, deciding to rely exclusively on PDPs (Partner Dematerialization Platforms) for invoice processing and delivery. The PPF (Portail Public de Facturation) will focus primarily on the central directory of PDPs (“Annuaire”) and the e-reporting aspects of the mandate. As a result, the French mandate will ultimately follow a 5-corner model.

This shift has notable implications, particularly for many companies (especially smaller ones) and service providers that had initially planned to rely solely on the PPF. These businesses will now need to adjust their approach and select a PDP.

For some companies, this may result in additional costs, as the PPF was initially a free option, whereas most PDPs will likely charge for their services.

As a result, PDPs will play a central role in the upcoming B2B mandate, as their use will be mandatory. This will enable them to showcase their unique capabilities. Already, various types of PDPs are emerging, such as international e-invoicing providers targeting large companies, local French providers focusing on smaller businesses, accounting solutions, banks, etc.

However, many uncertainties still persist. Several critical topics, such as Peppol interoperability and invoice lifecycle management between PDPs, have yet to be addressed in the official specifications.

To address these gaps, the French tax authority (DGFiP) has assigned an AFNOR commission (the French standardization body) to finalize the PDP specifications, while the future French Peppol Authority will be responsible for defining the PDP interoperability framework.

With less than two years remaining before the mandate takes effect, deadlines are getting tighter, and everyone hopes there won’t be another postponement, and that PDPs and companies will be ready on time.